By Vladymir Valentin | Realtor® | ABR, SRS, MRP

Serving Philadelphia, the Main Line, and South Jersey | Navy Veteran helping buyers and sellers move with a plan, not pressure

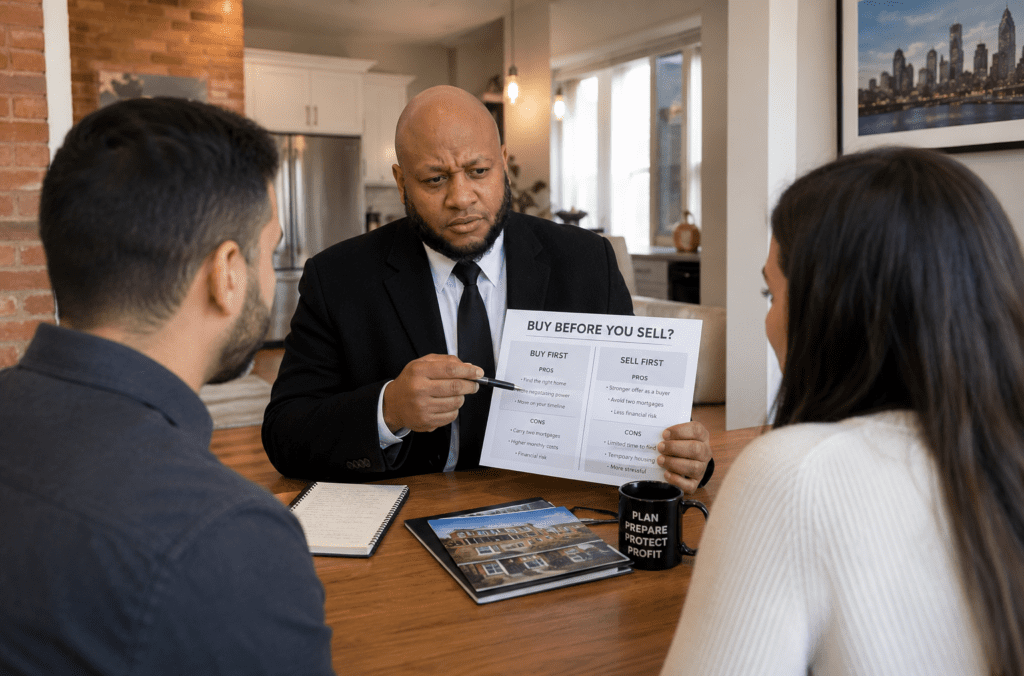

Philadelphia homeowners making a move in 2026 face the same high-stakes question: do you buy first and risk owning two homes, or do you sell first and risk having nowhere to go? With Philadelphia inventory at 4.2 months supply and homes averaging 35 days on market, both paths carry real consequences. This guide gives you a decision framework built on data, not guesswork.

Philadelphia Buy-Before-Sell Market Snapshot 2026

Conditions shaping this decision right now:

- Philadelphia inventory: 4.2 months supply

- Median days on market: 35 days

- Current rate for bridge financing: 7.5% to 8.5%

- Philadelphia appreciation rate: 3.2% annually

Why timing matters by neighborhood:

- Fishtown: 18 days on market, low risk of your sale lingering

- Graduate Hospital: 22 days on market, competitive buyer pool helps your sale

- Manayunk: 35 days, moderate timing risk

- Point Breeze: 38 days, slightly more sale timeline uncertainty

Philadelphia Seller Prep Timeline

Step 1: Understand the Core Risk of Each Path

Before choosing your sequencing in Philadelphia, you need to understand exactly what you are risking in each direction.

If you buy before you sell in Philadelphia:

- You may carry two mortgages simultaneously if your Philadelphia sale takes longer than expected.

- At 6.25% rates, a $350,000 Philadelphia mortgage costs approximately $2,156 per month in principal and interest. Carrying two is a real financial strain for most households.

- You do have negotiating strength as a buyer because you are not making a contingent offer.

If you sell before you buy in Philadelphia:

- You are a clean, non-contingent buyer with maximum negotiating power.

- You may need temporary housing if you cannot find your next Philadelphia or suburban home in time.

- Short-term rentals in Philadelphia typically run $2,500 to $4,500 per month depending on size and neighborhood.

- In this market, well-priced Philadelphia homes sell in 35 days or less, so your timeline has a real floor.

Philadelphia Multiple Offer Strategy

Step 2: Evaluate Your Financial Position

Your financial position determines which sequence is viable. In Philadelphia, this analysis needs to be specific.

- Do you have enough cash reserves to carry both properties? Calculate two full months of both mortgage payments plus Philadelphia property taxes and insurance. If that number threatens your emergency fund, you should not buy first.

- What is your current Philadelphia home equity? Owners in Fishtown and Graduate Hospital who bought pre-2022 are typically sitting on $100,000 to $200,000 in equity. This changes what is possible.

- Have you been pre-approved, not just pre-qualified? Philadelphia listing agents routinely reject contingent offers that lack strong pre-approval documentation. A full underwritten approval is your best tool.

- Can you qualify for the new home with your current mortgage still counting against you? Lenders use your full current payment in your debt-to-income calculation even if you intend to sell.

The Philadelphia Bridge Loan Option 2026

Bridge financing is the mechanism that allows Philadelphia homeowners to buy before they sell without selling under pressure.

| Bridge Loan Feature | What to Expect in Philadelphia 2026 |

| Rate | 7.5% to 8.5% above standard mortgage |

| Term | Typically 6 to 12 months |

| Loan amount | Up to 80% of your Philadelphia home’s value minus existing mortgage |

| Best for | Equity-rich Philadelphia homeowners in fast-moving neighborhoods |

| Risk | If Philadelphia sale takes longer than expected, carrying costs stack up |

Bridge loans make the most sense for Philadelphia sellers with substantial equity, a clearly sellable property in a fast neighborhood, and the income to carry both payments for 60 to 90 days if needed.

Step 3: Understand Philadelphia Contingency Offers in 2026

A contingent offer means your purchase of a new home is contingent on the sale of your existing Philadelphia property. This is a legitimate tool in a balanced market.

- Philadelphia sellers in a less competitive segment, such as a $600,000 plus property in the suburbs of the Main Line, are more likely to accept a contingent offer with a right of first refusal.

- Philadelphia sellers in hot neighborhoods like Fishtown and Point Breeze who are fielding multiple offers will typically reject contingent offers outright.

- A 72-hour kick-out clause is the standard contingency structure in Philadelphia. If the seller receives another offer, you have 72 hours to remove the contingency or lose the home.

- Working with a buyer who is pre-approved with a strong down payment and a realistic sale timeline gives a contingent offer the best possible shot in Philadelphia.

Philadelphia Buy-Sell Decision Matrix 2026

Buy first if:

- You are in a fast Philadelphia neighborhood (Fishtown, Grad Hospital, Manayunk) where your home will sell in under 30 days

- You have 3 or more months of carrying costs in reserve

- You have found the right Philadelphia home and cannot afford to wait

- Your lender has fully approved you with both properties on your debt-to-income

Sell first if:

- You are in a Philadelphia neighborhood with 40-plus day average market times

- Your budget is tight and two mortgage payments would cause financial stress

- You want maximum negotiating power as a buyer in a competitive Philadelphia neighborhood

- You have a reliable short-term housing option if needed

Use a bridge loan if:

- You have significant Philadelphia home equity, typically $150,000 or more

- Your current Philadelphia home is priced, prepped, and ready to list immediately

- You have found the right next home and the timing cannot wait

- You have a Philadelphia lender who moves quickly and you have the income to qualify for both

Philadelphia Mistakes in This Decision

- Assuming your Philadelphia home will sell in your preferred timeline. Even in a 35-day average market, individual properties vary. A row home needing work in Point Breeze moves slower than a renovated twin in Brewerytown. Know your specific comp history, not the citywide average.

- Making an offer without a clear plan for your current Philadelphia home. Philadelphia listing agents always ask. Walking into a negotiation without a documented plan weakens your position.

- Underestimating temporary housing costs. Philadelphia short-term rental inventory is limited. Assuming you can find a flexible month-to-month option quickly is a real risk, especially in desirable Philadelphia neighborhoods.

Top Philadelphia Buy-Sell Timing Questions 2026

Q: Can I buy in Philadelphia without selling my current home first? A: Yes, if you can qualify for both mortgages simultaneously. Your lender will run the numbers. Many Philadelphia homeowners can do this with solid equity and income.

Q: How long does it realistically take to sell in Philadelphia right now? A: Well-priced, well-prepared Philadelphia homes are averaging 35 days on market. From contract to closing adds another 30 to 45 days. Plan for 60 to 75 days from list to settlement.

Q: Is a sale contingency a dealbreaker in Philadelphia? A: In competitive price points and hot Philadelphia neighborhoods, yes, often. In the $650,000-plus segment or in neighborhoods with more inventory, sellers are more flexible. This is a conversation to have before you write any offer.

Philadelphia Market Report 2026

Ready to Make Your Philadelphia Move in the Right Order?

Philadelphia in 2026 rewards buyers and sellers who plan the sequencing before they act. Whether you buy first, sell first, or use bridge financing, the path that protects your finances and your timeline is the one that starts with accurate data about your specific Philadelphia neighborhood.

Let’s map out your Philadelphia buy-sell timeline today.

👉 Download Your Free 2026 Home Buyer’s Guide

Vladymir Valentin

Realtor® | ABR, SRS, MRP

TCS Group | Keller Williams Empower

(215) 444-3976

vladymir@kw.com

vvalentin@tcsgroup.com